I just received a few brochures from my finance industry friends about the upcoming Private Retirement Scheme. Currently I am quite busy with my work but heck since this involves money, it pique my interest.

Here is my teardown (A term the techies used. Its meaning is to rip something apart to know its inner workings. Since I am an Engineer, I would like to use that term here :D )

The PRS structure is quite simple as shown in the above graph. PPA will monitor all the transactions of the contributors. Where contributors are employer or willing individual contributors. PRS providers are entities that provide investment schemes aka unit trust investment for contributors. And a trustee will protect the monies invested in various PRS provider's scheme.

1. Currently the PRS are the following:

- American International Assurance Bhd;

- CIMB-Principal Asset Management Bhd;

- Hwang Investment Management Bhd;

- ING Funds Bhd;

- Manulife Unit Trust Bhd;

- Public Mutual Bhd; and

- RHB Investment Management Sdn Bhd.

2. Who can contribute?!

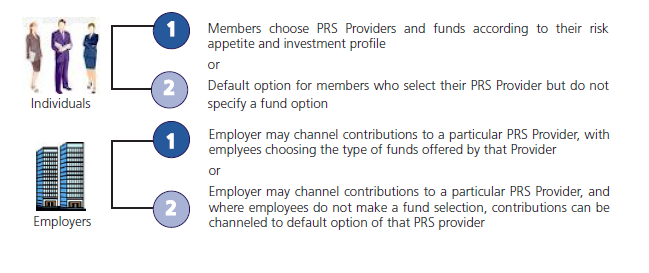

From the diagram above, individual can handpick which PRS provider scheme or fund that they want their money to be invested in. There is also a default option provided if someone have no idea what to invest in. I seriously doubt financial savvy contributors will choose default option.

Employers also can contribute on behalf of their employee but employee can choose which scheme to invest in. However, the info above seems to dictate that the employer have the privilege to select which PRS provider it "allows" the employee to invest it. The best option for employers is to give employee access to all the PRS providers. If not, this is not a good scheme as different employees have different strategy/favoritism/opinion where his/her money should go.

IMHO, employers contributing money into the PRS scheme is not a good enough incentive to retain or attract talent!! Because the next few points comes into the play.

3. When can a Contributor withdraw money from the PRS account?

− After the day the member reaches retirement age, which is currently 55; (Kris: My money is locked in for a long long time even though this is for retirement purposes)

− Following the death of a member;

− Permanent departure of a member from Malaysia; or

− For pre-retirement withdrawals.

• With respect to pre-retirement withdrawals, members may only withdraw the amount in sub-account B from each PRS Provider once a year. The first pre-retirement withdrawal can only be requested by a member one year after making the first contribution to any fund under the Scheme (whether the contribution is by an employer or member). While pre-retirement withdrawal may be made for any reason, a tax penalty of 8% on the withdrawal amount will be deducted by the PRS Providers before the balance is credited to the member’s account.

Kris: Sub-account B is 30% of the total money invested into the scheme. You cannot touch the other 70% until you hit 4 conditions above.

Wow!! 8% penalty is very very heavy! So don't simply withdraw just to buy your coach bag or the latest Iphone.

At least you can take out part of your money from EPF for 1st house (here is where you can roll your money. Shhh...) or education without incurring any penalties.

4. Is the return guaranteed like the EPF scheme?

Since your money is likely to be invested in unit trust or mutual funds, the returns are NOT guaranteed. I repeat again: NOT guaranteed!!

Kris: Hence EPF's solid GURANTEED 4-6% return is more attractive for those risk averse. You can also use part of EPF monies to invest in unit trust which returns are not guaranteed. But if you don't do that, you get the safe average 4-6% return.

5. What is the incentive for me or my employer to contribute to PRS?

- Individuals - tax relief of up to RM3,000; and

- Employers - tax deduction on contributions to PRS made on behalf of their employees above the statutory rate of up to 19% of employees’ remuneration for a period of 10 years.

A tax exemption is also provided on income received by the funds under the Schemes

Kris: Tax relief up to RM3,000 is quite a small amount, to be able to persuade me to lock my money up until I reach 55 years old. It will barely move my tax bracket to a lower bracket.

What We Don't Know Yet?? Question Marks??

1. What are the minimum charges (service charge, switching fees) that needs to be incurred when investing in a fund provided by PRS providers. I hope that is LOWER or at least match the rates offered when a person uses the EPF money to invest in mutual funds. Else, it is NOT very attractive to be in the PRS scheme. It is better to invest yourself in unit trust hence you are not limited to the retirement age withdrawal restrictions & possibly the 8% penalty!!

There should be also management fees incurred by the Scheme Trustees besides the normal unit trust management fees. Not sure how much the Scheme Trustee gets?? And also the PPA also needs to be paid.

2. When is the PRS scheme is going to be implemented?? See some feedback first?? Perhaps I should submit my feedback based on this blog post :D

3. I hope that PPA's online system is very robust and user friendly since it is up to the PPA to track a contributor's investment in multiple PRS providers's scheme. Here the PPA needs to maintain a central database of all the contributors' investment activities.

4. Employers of huge companies would need a payroll system upgrade if it wants to contribute part of the money into the PRS since it involves taxes implications, tracking employee's PRS account, etc. And if they add in vesting restrictions (as suggested by the brochure), it is going to be very complicated to handle! Not many small & medium enterprise would have the resources to do so. Backend system between employers and PPA needs to be comprehend.

Conclusion: Disclaimer, my opinion as solely mine and not intended as financial advice :D .

The PRS scheme really needs to add more sugar and candy bars to entice me to contribute! It will lock my money for a long time with high withdrawal penalties and also the RM3,000 tax relief is NOT ENOUGH to offset this major disadvantage. Besides that my returns are not guaranteed, and I could lose money if my unit trust picks turns sour. Worst still ,the default option is not satisfactory. At least I get a secure albeit small return from EPF.

And for employers, if employees in general don't want to invest in PRS, this is going to save them alot of resources needed to update their payroll system to cater to PRS.

Yea, I think savvy investors like yourself won't even bothered after looking these details :)

But yea, 8 percent is just seriously absurd.

Haha.. I don't think this scheme will flight off. It is too unfavorable.

The return should be pretty conservative like EPF, no?

Not entirely, ChampDog. The reason is that they invest in unit trusts. And unit trusts returns can fluctuate over the market cycles. So it is not conservative at all compared to our "safe" EPF unless you pick a savings or bond unit trust.

I think it makes sense if you tax bracket at least 19%. With EPF return of 4-5%, you already break even after 4 years, even though you don't gain anything from the unit trust investment.

Foo,

I believe most people don't wait to for 4 years just to break even with their investment :D

Life is too short.